Many investors unknowingly concentrate too much of their portfolio in domestic stocks - a behavior known as home bias. This creates unnecessary risk and limits potential returns. By rebalancing your portfolio regularly and diversifying globally, you can reduce these risks and align your investments with long-term goals.

Key Takeaways:

- Rebalancing: Adjust your portfolio periodically to maintain your target asset allocation and risk level.

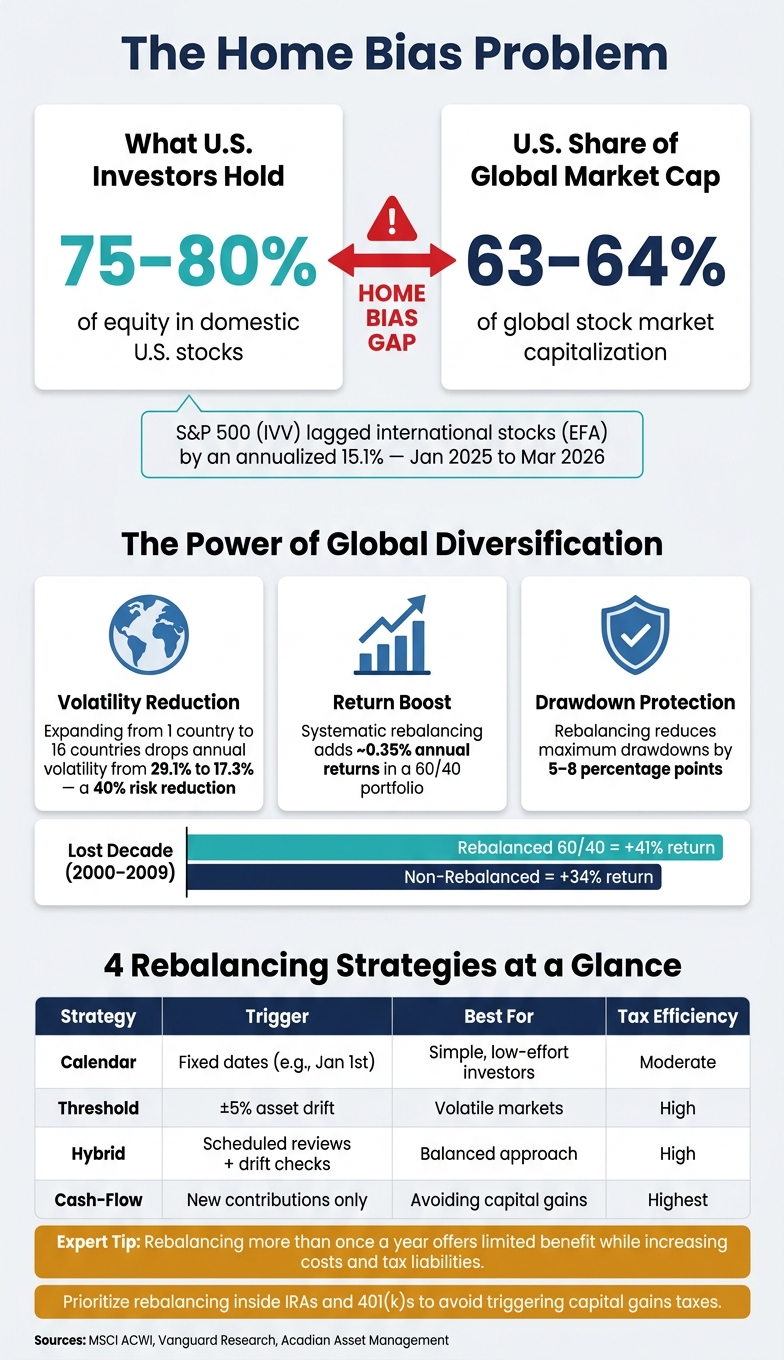

- Home Bias: U.S. investors allocate 70-76% of their equity to domestic stocks, despite the U.S. representing only 63-64% of global market capitalization.

- Diversification Benefits: Adding international investments lowers volatility and can improve returns without increasing risk.

- Strategies: Use tools like threshold-based rebalancing (e.g., ±5% drift) or cash-flow rebalancing to maintain balance while minimizing taxes and transaction costs.

By addressing home bias and rebalancing strategically, you can build a more resilient portfolio that performs better across different markets and economic conditions.

Home Bias vs. Global Diversification: Key Stats & Rebalancing Strategies

Recognizing and Addressing Home Bias

Common Causes of Home Bias

Home bias often stems from habits and natural preferences that shape investment decisions.

One major factor is familiarity bias - investors tend to favor brands and services they encounter regularly. As Motley Fool Asset Management explains: "Recognizing the logo on a storefront doesn't mean a company's stock will outperform the market." Additionally, some investors - especially men - display overconfidence, believing they have special insights into domestic companies, even when this belief is unsupported.

Economic factors also contribute. Many investors prefer domestic assets to mitigate risks like local inflation or to avoid the complexities of foreign investments. Holding assets in euros or yen, navigating unfamiliar tax regulations, and keeping up with international news can feel overwhelming and not worth the effort. This cautious mindset often leads to portfolios that are too concentrated in domestic markets.

Understanding these behaviors is key because they directly tie into the risks associated with home bias, which we'll explore next.

Risks of Home Bias in Portfolios

A major drawback of home bias is concentration risk. Portfolios heavily tilted toward a single country's economy are more susceptible to that nation's political changes, interest rate shifts, and sector-specific downturns.

For instance, between January 20, 2025, and March 18, 2026, the S&P 500 (IVV) lagged behind international stocks (EFA) by an annualized 15.1%. Investors with diversified global portfolios fared better during this period compared to those focused on U.S. equities.

Another risk is the multinational fallacy. Many assume that owning shares in U.S. multinationals like Procter & Gamble or Coca-Cola provides sufficient global diversification. However, these companies' stocks are still traded on U.S. exchanges, making them heavily influenced by domestic interest rates, market sentiment, and currency fluctuations. Global revenue streams don’t necessarily translate to true international diversification.

"A strong portfolio isn't built around one country winning forever. It's built to remain resilient across different markets, environments, and economic cycles." - Jason Blumstein, CFA

How to Diagnose Home Bias in Your Portfolio

Once you understand the causes and risks, the next step is to assess your portfolio for signs of home bias.

Start by comparing your domestic allocation to global market cap weights. As of early 2026, the U.S. accounts for about 47.3% of global stock market capitalization. If more than 70% of your portfolio is in U.S. equities - a common scenario - it’s a clear indicator of home bias.

Next, review your sector allocation. Look for overweights in dominant U.S. sectors like large-cap technology and underweights in international sectors such as financials, materials, or energy. Dig into your holdings to uncover any hidden domestic tilt.

Lastly, take a closer look at your tax-deferred accounts. IRAs and 401(k)s are excellent tools for rebalancing toward international holdings since adjustments within these accounts don’t trigger capital gains taxes. If selling isn’t an option, consider directing new contributions to underrepresented international asset classes. This gradual shift can help balance your portfolio without immediate tax consequences.

Rebalancing for Diversification

How Rebalancing Reduces Home Bias

Rebalancing is a key tool for maintaining diversification, especially when addressing home bias. Over time, domestic assets that perform well can grow disproportionately in your portfolio, leading to an unbalanced allocation. Rebalancing helps realign your investments by shifting funds toward underweight international assets, reducing concentration risks. This process enforces the principle of "sell high, buy low", which can be emotionally challenging but is essential for maintaining balance. As Ryan O'Connell, CFA, FRM, explains:

"Portfolio rebalancing is not about maximizing returns - it's about maintaining your intended level of risk exposure."

One effective way to rebalance is through cash-flow rebalancing, where new contributions are directed toward underweight areas, like international assets. This approach helps restore balance without triggering capital gains taxes.

Rebalancing not only corrects allocation drift but also prepares you to select a strategy that aligns with your investment style.

Rebalancing Strategies

When choosing a rebalancing strategy, it’s important to consider your management preferences and sensitivity to transaction costs. Here are some common approaches:

| Strategy | Trigger | Best For |

|---|---|---|

| Calendar | Fixed dates (e.g., every January 1st) | Investors who prefer a simple, low-effort plan |

| Threshold | When assets deviate by a set percentage (e.g., ±5%) | Markets with frequent fluctuations |

| Hybrid | Scheduled reviews with drift checks | Balancing minimal trades and avoiding large imbalances |

| Cash-Flow | New contributions | Rebalancing without selling existing winners |

A hybrid strategy often strikes a good balance between minimizing trades and keeping your portfolio aligned. For example, quarterly reviews combined with trades only when an asset drifts beyond a 5% threshold can help reduce transaction costs while maintaining balance. Research shows that rebalancing more frequently than once a year offers limited additional benefits while increasing costs and potential tax liabilities.

When rebalancing, prioritize tax-advantaged accounts to avoid creating taxable events.

Simulating Rebalancing in Virtual Portfolios

Before applying a rebalancing strategy to your actual investments, it’s a good idea to test it in a simulated environment. For example, during the "Lost Decade" (2000–2009), a 60/40 portfolio that was rebalanced annually achieved a 41% return, compared to 34% for a portfolio that wasn’t rebalanced. Without rebalancing, the portfolio would have drifted into a much riskier allocation, especially leading up to the 2008 financial crisis.

Platforms like For Traders allow you to experiment with different strategies using virtual capital. These demo accounts let you test rebalancing thresholds - such as 5% versus 10% drift limits - under various market conditions. Simulated trading offers a risk-free way to see how your chosen strategy might perform during volatile periods, helping you gain confidence before implementing it in your real portfolio.

Practical Steps to Achieve Diversification

Setting Target Allocations

To start, align your portfolio with a global benchmark. For example, as of mid-2026, the U.S. accounts for about 63% of the MSCI All Country World Index (ACWI). However, the typical U.S. investor holds 75% to 80% in domestic stocks, showcasing a clear home bias. Adjusting for this bias helps distribute risk more effectively.

Experts often recommend allocating 20% to 40% in international equities to reduce geographic concentration. Additionally, keep an eye on sector concentration. For instance, technology represents over 32% of the S&P 500 but only about 14% of markets outside the U.S. Diversifying internationally can naturally balance this exposure.

When deciding on your stock-to-bond mix, the "120 minus age" rule can be a helpful guide. For example, a 30-year-old might aim for 90% stocks and 10% bonds, while a 60-year-old might shift to 60% stocks and 40% bonds. From there, incorporate your geographic allocation targets into the mix.

Implementing Rebalancing Rules

Once your target allocations are set, establish clear rules to maintain them. Start by directing new contributions to underweight assets. For instance, if your international allocation has fallen below target, consider channeling your next deposit into a low-cost international ETF, like Vanguard Total International Stock ETF (VXUS) or iShares Core MSCI Total International Stock ETF (IXUS), both with a 0.07% expense ratio. This approach avoids selling assets and helps you sidestep capital gains taxes.

If selling assets becomes necessary, prioritize doing so in tax-advantaged accounts like IRAs or 401(k)s. In taxable accounts, look for opportunities to harvest losses on underperforming positions (e.g., long-term government bond funds, which have seen notable losses in recent years) to offset any realized gains.

To minimize transaction costs, set a minimum trade size, such as $500 or $1,000.

Measuring Progress Toward Diversification

After rebalancing, it's essential to monitor progress to ensure your portfolio stays aligned with your diversification goals. Focus on three key metrics:

- Portfolio drift: This measures how far your current allocations have strayed from your targets. For example, if your international allocation was set at 30% but has dropped to 23%, that 7% drift likely requires action, especially under a ±5% threshold rule.

- Volatility and drawdown: Diversification should help reduce losses. Historically, adding international stocks has lowered portfolio volatility by 1 to 2 percentage points annually. Maximum drawdown, which tracks the largest decline from peak to trough, is another useful measure. Research indicates that global diversification reduced drawdowns by 22% before 1998 and by 14% after 1998, as global market correlations have increased.

-

Correlation: Monitoring the correlation between domestic and international assets is crucial for assessing diversification. As Acadian Asset Management explains:

"It has been said that diversification is the only free lunch in finance. While the free lunch of global diversification is always valuable, it becomes especially nutritious when markets fragment and correlations decline."

During market crises, correlations often spike, reducing the benefits of traditional diversification. In such cases, alternative assets like gold, commodities, or TIPS can help fill the gap.

Monitoring and Risk Management Over Time

Tracking Portfolio Drift

Keeping your portfolio diversified takes regular monitoring and adjustments. Over time, as different assets grow at varying rates, your portfolio can stray from its original allocation. For example, a 60/40 stock-bond portfolio started in 2010 would have shifted to about 80/20 by 2024, largely due to U.S. equity outperformance - a major change in risk exposure that often goes unnoticed by investors.

To stay on track, review your allocations every quarter and make adjustments only when there's a 5% deviation from your target. This threshold is widely accepted: if a 30% allocation drops below 25% or exceeds 35%, it’s time to rebalance. Research from Vanguard supports this approach as a way to balance risk control with minimizing transaction costs. Also, make sure to monitor your entire portfolio, including both taxable and tax-advantaged accounts. For instance, your international equity exposure might seem fine in your IRA, but if your 401(k) is heavily weighted toward domestic stocks, your overall diversification could be off.

In addition to tracking drift, it’s important to stress test your portfolio to prepare for potential regional market shocks.

Stress Testing for Regional Risks

Stress testing helps you understand how your portfolio might handle regional market disruptions. Start by conducting a "look-through" review to uncover hidden overlaps. This means going beyond fund-level percentages to see if multiple holdings are tied to the same companies or sectors. For example, as of April 2026, five mega-cap U.S. stocks made up about 23% of the broad U.S. market index, highlighting a significant concentration risk for many investors who believed they were diversified.

Consider scenarios like a 20% drop in U.S. equities while international markets remain steady, or vice versa. In March 2026, the MSCI World Index experienced a 6.55% decline before rebounding by 10.1% in April, showing how quickly concentration risk can lead to real losses for a portfolio that has drifted. If a single-region downturn would result in losses beyond your comfort level, it’s a sign that your geographic diversification needs improvement.

"Rebalancing is the process of restoring a portfolio to its intended risk profile by returning asset class weights to their target allocations. It is a risk management discipline, not a market forecast." - John Zadeh, CEO, StockWire X

When you rebalance, document your decisions. Include the date, current allocations, and the reason for acting (or not acting). This creates a clear record and helps remove emotional bias from future decisions.

For a hands-on approach, consider using tools designed to simulate and manage portfolio diversification.

Using For Traders Resources to Stay Diversified

For Traders provides a range of tools to help traders maintain diversification and manage risks effectively in simulated portfolios:

- Portfolio Health Checker: Powered by TradingGrader, this tool lets you input stock tickers or crypto symbols to receive a health score (0–100). It flags issues like concentration risk, drawdown exposure, and compares your holdings to benchmarks like the S&P 500 and NASDAQ. It's a quick way to identify hidden biases before they become problems.

- 40% Margin Rule: This feature limits any single instrument to 40% of total margin, reducing the risk of over-concentration at the trade level.

- Automated Drawdown Protection: Automatically closes trades if losses hit -2% of the starting balance, ensuring discipline during volatile market conditions.

- Access to 100+ Assets: From Forex and indices to commodities and over 50 cryptocurrencies, you can create diversified, multi-region exposure all within one account.

These tools provide practical ways to refine and manage your portfolio, ensuring it stays aligned with your goals and risk tolerance.

Breaking the Home Bias and Rethinking International Exposure | Future Proof Insights

Conclusion and Key Takeaways

Home bias is a common and often underestimated risk in investment portfolios. U.S. investors, for instance, tend to allocate about 76% of their equity to domestic stocks, even though the U.S. accounts for only 63–64% of global market capitalization. This overconcentration can lead to heightened risk over time.

One effective way to address home bias is through regular rebalancing. As Ryan O'Connell, CFA, FRM, puts it:

"Portfolio rebalancing is not about maximizing returns - it's about maintaining your intended level of risk exposure."

A balanced strategy, like quarterly reviews paired with a 5% drift threshold, can encourage action without leading to excessive trading. Additionally, directing new contributions toward underweight international assets can help maintain a diversified portfolio.

The advantages of diversification are undeniable. Expanding from a single-country portfolio to one that spans 16 countries can lower annual volatility from 29.1% to 17.3% - a 40% drop in risk. Furthermore, systematic rebalancing has been found to boost annual returns by approximately 0.35% in a 60/40 portfolio while reducing maximum drawdowns by 5–8 percentage points. These figures underscore the importance of rebalancing in mitigating home bias and maintaining a healthy, well-rounded portfolio.

FAQs

How much international stock should I own?

When deciding how much to invest in international stocks, it largely depends on your financial goals and how much risk you're comfortable taking on. Many experts recommend using global market-capitalization weights as a starting point. Currently, the U.S. accounts for about 60%-70% of the global equity market, which leaves 25%-30% for non-U.S. equities as a commonly suggested allocation. This mix helps diversify your portfolio, reducing risk and avoiding too much dependence on just one market.

When should I rebalance to fix home bias?

To tackle home bias, it's important to rebalance your portfolio whenever its allocation drifts away from your target. There are a few common approaches to this:

- Calendar approach: Review your portfolio annually, regardless of market conditions.

- Threshold approach: Rebalance only when an asset's allocation shifts by a specific percentage.

- Hybrid approach: Combine both methods - review on a set schedule, but only make changes if the drift surpasses your chosen threshold.

Pick the strategy that fits your goals while maintaining proper diversification.

How do I rebalance without big tax hits?

When rebalancing your investments, there are ways to keep taxes low. Start by focusing on tax-advantaged accounts like IRAs, 401(k)s, or HSAs. Trades in these accounts don’t trigger capital gains taxes, making them ideal for adjustments.

In taxable accounts, consider redirecting new contributions, dividends, or interest to assets that are underweighted. This approach avoids selling and minimizes taxable events. If selling is unavoidable, tax-loss harvesting can help. By selling investments at a loss, you can offset gains elsewhere, reducing your tax burden.

Finally, rebalancing less often - such as once a year - can further limit the number of taxable events, keeping your tax liability in check.

Related Blog Posts

Start Trading with For Traders

Join our platform to test your trading skills, trade virtual capital, and earn real profits. Access educational resources, advanced tools, and a supportive community to enhance your trading journey.

Start your Trading Challenge