Dynamic portfolio rebalancing adjusts investments based on market conditions instead of sticking to fixed schedules. It reacts to changes like asset allocation drift or economic shifts, helping you maintain your desired risk level. Unlike static rebalancing, which operates on a set timeline, dynamic rebalancing is flexible and event-driven, offering better responsiveness to market volatility.

Key Points:

- Dynamic Rebalancing: Adjusts when allocations deviate from targets (e.g., ±5% drift).

- Static Rebalancing: Follows fixed intervals (e.g., quarterly or annually).

- Benefits: Helps manage risk, avoids emotional decision-making, and improves alignment with financial goals.

- Common Strategies: Threshold-based, hybrid (schedule + drift), and market condition-based methods.

Dynamic rebalancing is especially useful in virtual trading platforms, where automated tools can monitor and adjust portfolios in real time. This approach ensures portfolios stay aligned with risk parameters, even during market turbulence.

Portfolio Rebalancing Explained | Strategies, Timing, & Risk Management

Dynamic vs Static Rebalancing

Dynamic vs Static Portfolio Rebalancing: Key Differences and Benefits

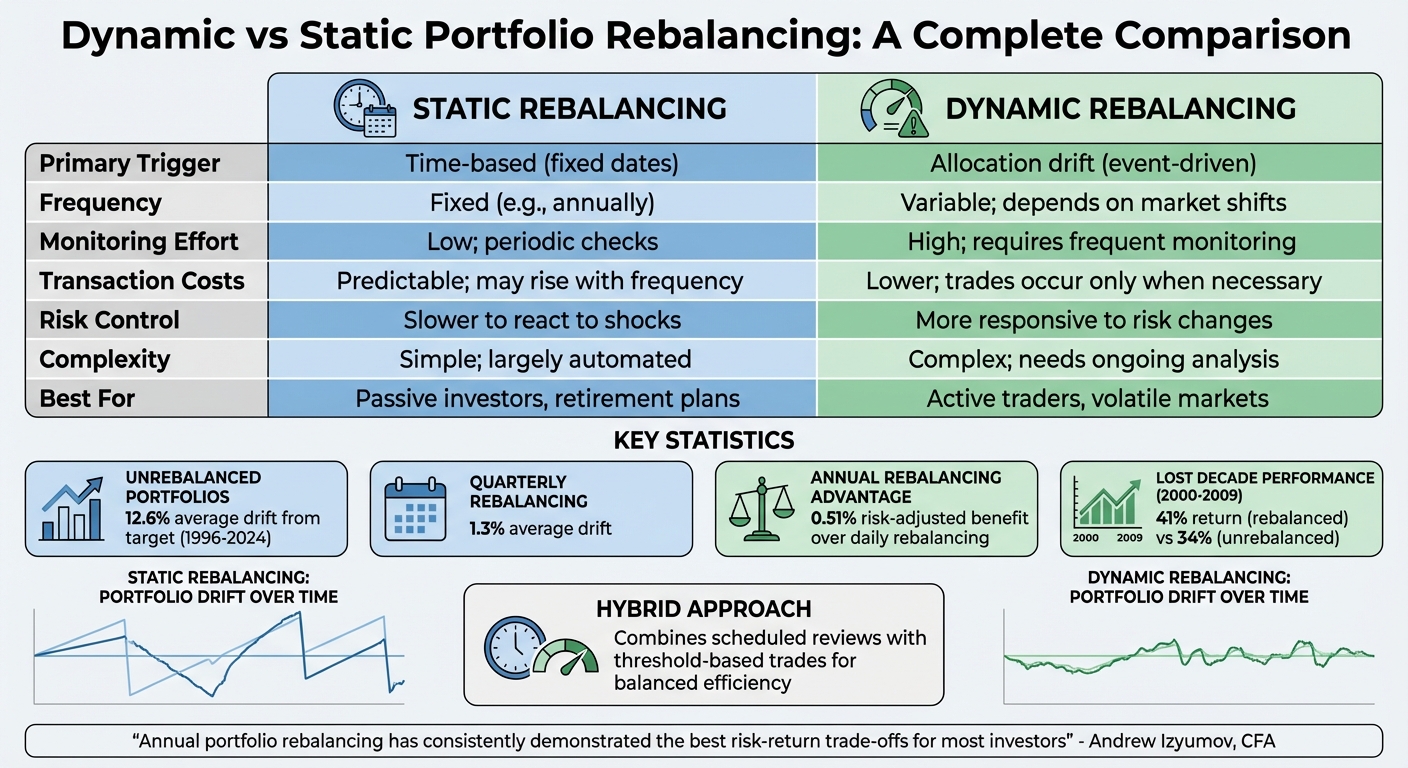

The main distinction between these two methods lies in how they are triggered. Static rebalancing follows a fixed schedule - whether that's monthly, quarterly, or annually - without considering market conditions. Even during extreme market swings, this method waits for the pre-determined date to make adjustments.

On the other hand, dynamic rebalancing is activated when an asset strays from its target allocation by a specific threshold, like 5%. This makes its timing unpredictable. For instance, in highly volatile markets, you might rebalance several times in one month. Conversely, in calmer periods, your portfolio could remain untouched for years.

A hybrid approach combines scheduled reviews with threshold-based trades, offering a balance between disciplined timing and cost efficiency. This model allows for a structured review process while reducing the need for constant monitoring. Static rebalancing is ideal for those seeking minimal daily oversight, whereas dynamic rebalancing requires more frequent checks to catch deviations. As Andrew Izyumov, CFA and Founder of 8FIGURES, explains:

Annual portfolio rebalancing has consistently demonstrated the best risk-return trade-offs for most investors and financial advisors alike.

The difference between these strategies becomes clear when you look at the data. A study spanning 29 years (1996–2024) revealed that portfolios left unrebalanced drifted an average of 12.6% from their target allocation. Meanwhile, portfolios rebalanced quarterly kept an average drift of just 1.3%. Annual rebalancing provided a risk-adjusted advantage of 0.51% over inefficient daily rebalancing. These findings highlight how rebalancing frequency impacts both performance and risk control, as summarized in the table below.

Comparison Table: Dynamic and Static Rebalancing

| Feature | Static Rebalancing | Dynamic Rebalancing |

|---|---|---|

| Primary Trigger | Time-based (e.g., fixed dates) | Allocation drift (event-driven) |

| Frequency | Fixed (e.g., annually) | Variable; depends on market shifts |

| Monitoring Effort | Low; periodic checks | High; requires frequent monitoring |

| Transaction Costs | Predictable; may rise with frequency | Lower; trades occur only when necessary |

| Risk Control | Slower to react to shocks | More responsive to risk changes |

| Complexity | Simple; largely automated | Complex; needs ongoing analysis |

| Best For | Passive investors, retirement plans | Active traders, volatile markets |

| Simulated Prop Trading | Consistent long-term risk management with minimal effort | Ideal for strict drawdown management |

Benefits of Dynamic Rebalancing in Virtual Portfolios

Dynamic rebalancing takes risk management in virtual trading to the next level. Its key strength lies in maintaining your portfolio's target allocation, even as markets fluctuate. For example, without rebalancing, a 60/40 stock–bond portfolio can shift to a much riskier 70/30 allocation during market rallies, undermining your original strategy.

The impact on performance is clear. Take the "Lost Decade" (2000–2009): a 60/40 portfolio rebalanced annually delivered a 41% return, compared to just 34% for an unrebalanced portfolio. That 7% gap highlights how disciplined rebalancing, often involving contrarian trades, can make a significant difference. These results make dynamic rebalancing particularly effective in virtual trading scenarios.

Platforms like For Traders amplify these benefits in simulated environments. Without real-world constraints like transaction fees or capital gains taxes, traders can implement aggressive ±5% threshold strategies without worrying about profit erosion. Additionally, For Traders enforces a strict 5% drawdown threshold, triggering automatic rebalancing to manage risk exposure. These features enhance both risk management and learning opportunities for users.

Research spanning 8,585 equity funds from 1999 to 2015 shows that professional fund managers consistently rely on rebalancing to adapt to market shifts while maintaining their strategic allocations. As Finzer puts it:

Portfolio rebalancing is fundamentally a risk-control tool, not a return-chasing tactic. Its main job is to ensure the risk profile you chose is the one you actually have.

This approach also reduces emotional decision-making, which can derail trading strategies during volatile periods.

For virtual trading, the ability to respond instantly is game-changing. Instead of waiting for quarterly reviews, dynamic rebalancing adjusts your portfolio the moment an asset class moves beyond your set threshold. This real-time responsiveness is essential on platforms like For Traders, where consistent risk management directly affects your ability to hit profit targets and qualify for bi-weekly payouts.

Key Strategies for Dynamic Portfolio Rebalancing

Selecting the right rebalancing strategy hinges on your trading style, access to automation, and tolerance for transaction costs. Each method offers distinct ways to maintain your target allocation and manage risk. For those using simulated platforms and prop firms, picking the right dynamic strategy is essential for effective real-time risk management and skill-building.

Threshold-Based Rebalancing

Threshold-based rebalancing triggers trades when an asset's weight strays from its target by a predefined percentage. Unlike calendar-based methods, this strategy responds solely to portfolio drift. For instance, with a ±5% threshold on a 30% equity allocation, you’d rebalance only if the equity position drops below 25% or rises above 35%.

The 5/25 Rule is a handy guideline: rebalance when an asset class shifts by 5 percentage points in absolute terms or by 25% of its target weight in relative terms, whichever is smaller. This approach is especially effective for automated systems.

Research highlights a key insight: rebalancing less often than every two weeks reduces the strategy’s effectiveness. Michael Kitces, Head of Planning Strategy at Buckingham Wealth Partners, reinforces this:

Checking less often – particularly any less frequently than once every 2 weeks (every 10 trading days) – resulted in diminishing rebalancing benefits.

This strategy shines in volatile markets, where automated systems can seize "buy-low, sell-high" opportunities immediately. For portfolios with smaller holdings (5-10% each), relative bands ensure fair trade triggers across all asset sizes.

While threshold rebalancing is highly responsive, it can lead to frequent trades during market turbulence. A hybrid approach adds structure while maintaining flexibility.

Hybrid Periodic-Threshold Rebalancing

Hybrid rebalancing blends fixed schedules with drift triggers, balancing structure and efficiency. You review your portfolio at specific intervals - like quarterly or semi-annually - but only rebalance if asset allocations exceed your set thresholds.

This method reduces the need for constant monitoring. For example, you might check your portfolio and find only minor drift (1-2%), allowing you to skip unnecessary trades.

| Feature | Threshold-Based Rebalancing | Hybrid Periodic-Threshold |

|---|---|---|

| Primary Trigger | Deviation from target weight (Drift) | Time interval + Deviation threshold |

| Monitoring | Continuous or high-frequency | Scheduled (Quarterly/Semi-annually) |

| Responsiveness | High; reacts immediately to market moves | Moderate; reacts only at check dates |

| Transaction Costs | Variable; high in volatile markets | Lower; avoids minor adjustments |

| Best For | Automated/Active traders | Manual/Cost-sensitive investors |

Vanguard offers timeless advice here:

The most important thing is that you settle on a rule that you can stick to.

Hybrid rebalancing is ideal for those who prefer a structured routine without the hassle of constant oversight.

Market Condition-Based Rebalancing

Market condition-based rebalancing adapts your target asset mix based on medium-term forecasts or risk indicators instead of fixed allocations. This method accounts for shifts in volatility, interest rates, or broader economic trends.

Consider the 2020-21 tech boom: this strategy would have encouraged selling overheated sectors at their peak while buying lagging ones - helping avoid over-concentration during market euphoria. Without rebalancing, a 60/40 equity/bond portfolio from 1989 would have drifted to 80% equities by 2021, significantly raising its risk.

From January 2008 to May 2024, Alquant tested a "Combined Indicator" strategy on an S&P 500 and USD cash portfolio. Using a 66% risk threshold to shift fully to cash, the approach averaged just 4.1 rebalancing actions per year while delivering 5% alpha and better Sharpe and Calmar ratios compared to a semi-annual 50/50 benchmark.

To apply this strategy, keep an eye on macro indicators like interest rates, inflation expectations, and global growth. Tools like the VIX, Alquant Vega Indicator, or Sahm Rule can signal shifts to safer assets like cash or bonds. In volatile markets, narrower tolerance bands can limit risky exposures, while wider bands help reduce transaction costs caused by frequent trades.

This approach emphasizes discipline and risk management over chasing returns.

Risk-Based Rebalancing

Risk-based rebalancing focuses on maintaining your desired risk level rather than maximizing returns. As Vanguard succinctly puts it:

The purpose of rebalancing is to manage risk, not maximize returns.

This strategy becomes critical when your circumstances change. For example, if you’re nearing a withdrawal deadline, you’ll need more conservative rebalancing to protect against sequence-of-returns risk. A classic example is Constant Proportion Portfolio Insurance (CPPI), which reduces exposure to risky assets as portfolio values approach a defined "floor", reallocating funds into safer options like Treasuries or cash.

In a simulated 30% equity market drop, a rebalanced portfolio lost $0.2 million less than an unrebalanced 60/40 portfolio. Research from T. Rowe Price (1998-2023) found that wider tolerance bands (e.g., 3% fixed or 25% relative) reduced transaction costs while still mitigating bear market risks.

Define a "floor" value in dollar terms to guide your risk tolerance. For instance, increase risky asset exposure when your portfolio rises above the floor, and shift to safer assets as it nears the floor. Over 25 years of data, a 20% relative rebalancing band kept equity exposure within 5% of its original target.

Cash Flow and Opportunistic Rebalancing

Cash flow rebalancing uses new contributions, dividends, or interest to restore your portfolio's balance without selling existing positions. This approach minimizes transaction costs and avoids triggering capital gains taxes in taxable accounts.

Instead of selling high-performing assets, direct incoming cash toward underweight categories. For instance, if equities drift from 60% to 65%, use your next deposit to buy bonds and restore balance. This method is particularly effective for those with regular contributions or steady dividend income.

Optimize across accounts to boost tax efficiency. Aggressively rebalance in tax-deferred accounts like IRAs or 401(k)s, where trades don’t create taxable events. For taxable accounts, rely on cash flow adjustments to maintain your allocation while minimizing tax liabilities.

Implementing Dynamic Rebalancing Algorithms

To put rebalancing theory into action, start by creating a clear framework. Begin by defining your target asset allocation - this serves as your baseline for adjustments. For example, you might aim for 60% stocks and 40% bonds, depending on your risk tolerance and investment goals. This allocation acts as the foundation for every adjustment your algorithm will make.

Next, focus on choosing rebalancing triggers. These can be based on time intervals (monthly or quarterly), threshold deviations (e.g., ±5% from the target), or a combination of both. Most industry standards recommend thresholds between 3% and 5% deviation. However, for high-volatility assets like tech stocks, you might widen these bands to 7–10% to avoid excessive trading costs. Once your target allocation and triggers are set, the algorithm can continuously monitor and adjust the portfolio.

Real-time portfolio drift monitoring is key. Data feeds like the Yahoo Finance API provide the updates your algorithm needs. The algorithm then calculates adjustments, determining the exact number of shares to buy or sell. You can program it for full alignment, minimal corrections, or methods that preserve value.

When it comes to executing trades, aim for tax efficiency. Allocate new capital to underweight assets in taxable accounts to minimize short-term capital gains. Save more aggressive rebalancing for tax-advantaged accounts like IRAs, where trades don’t immediately trigger tax liabilities. Research on 8,585 equity funds from 1999 to 2015 shows that professional managers consistently adjust portfolios to align with their strategic allocations. For simulated prop trading, platforms like For Traders benefit from this algorithmic precision, ensuring that portfolios stay within strict risk parameters.

Steps to Set Up Dynamic Rebalancing

Building an effective rebalancing system requires both strategy and technical execution. Python integration is a great starting point. Libraries like yfinance can fetch real-time prices, while numpy handles numerical weight calculations. For portfolio optimization, tools like PyBroker and Riskfolio-Lib are particularly useful, offering features like minimizing Conditional Value at Risk [[29]](https://www.pybroker.com/en/latest/notebooks/9. Rebalancing Positions.html).

Set up automated triggers using APIs. Platforms like Alpaca allow you to create portfolios with specific cash and stock percentage weights that automatically update based on your chosen triggers. For example, you could set a 10% drift threshold, triggering a rebalance regardless of the time elapsed. To avoid over-trading in volatile markets, implement a cooldown period - a 7-day gap after each rebalance can help.

Carefully manage friction and costs. Frequent rebalancing can lead to higher transaction fees, bid-ask spreads, and slippage, all of which erode returns. Monthly rebalancing, for instance, can result in turnover rates two to four times higher than quarterly methods. Ensure you maintain enough cash for minimum orders to prevent partial or failed rebalancing attempts.

These strategies form the backbone of a systematic rebalancing process. For users of For Traders virtual capital plans (ranging from $6K to $100K), algorithmic rebalancing ensures strict adherence to risk parameters. The platform’s AI-driven tools provide 24/7 tracking and smart alerts whenever allocations drift beyond preset thresholds. Coupled with a 5% maximum drawdown limit, automated rebalancing allows traders to focus on their strategies while keeping portfolios within acceptable risk boundaries.

| Rebalancing Method | Trigger Mechanism | Primary Benefit | Best For |

|---|---|---|---|

| Time-Based (Calendar) | Fixed intervals (Monthly, Quarterly, Annual) | Simple, low monitoring, removes emotion | Busy, long-term investors |

| Threshold-Based (Drift) | Deviation from target % (e.g., ±5%) | Responsive to market changes, tight risk control | Proactive risk management |

| Volatility-Based | Portfolio volatility exceeds a set limit | Dynamic risk management in choppy markets | Sophisticated algorithmic traders |

| Hybrid | Fixed schedule + Threshold breach | Balanced discipline and flexibility | Practical middle ground |

Finally, keep an eye on account restrictions that could block automated execution. Issues like Pattern Day Trading (PDT) flags, ACH returns, or high position-to-equity ratios (above 6:1) can interfere with your algorithm. Configure alerts to notify you of these problems immediately. Research shows that annual rebalancing can yield a risk-adjusted benefit of 51 basis points (0.51%) compared to inefficient daily rebalancing. This highlights how strategic timing often outperforms constant portfolio tweaking.

Dynamic Rebalancing in Simulated Prop Trading on For Traders

In simulated prop trading, dynamic rebalancing plays a critical role - not just in optimizing returns but also in safeguarding virtual capital. For Traders enforces strict risk parameters across its virtual capital plans, which range from $6,000 to $100,000. Without consistent rebalancing, portfolios can drift into riskier allocations during bull markets, potentially violating these parameters and exposing traders to unnecessary risks.

For Traders connects seamlessly with platforms like MetaTrader 5, cTrader, and TradeLocker. These integrations provide advanced charting tools, technical indicators, and fast execution, making systematic rebalancing more efficient. The platform's dashboard delivers real-time insights and includes a trading journal, helping traders identify portfolio drift early and take corrective action before drawdown limits are breached. This functionality also supports the platform's evaluation process, which prioritizes disciplined risk management.

"At For Traders, everything is designed around you the trader. Transparent objectives, flexible conditions, fast payouts, and the most intuitive dashboard in the industry come together to create an environment where skills truly scale."

The platform's two-phase evaluation structure further emphasizes the importance of disciplined rebalancing. In Phase 1 (Evaluation), traders must achieve a 9% profit target while adhering to strict drawdown rules. Phase 2 (Master Account) allows for scaling virtual capital over time, provided traders maintain consistent risk control. The simulated nature of the environment also eliminates capital gains taxes, enabling frequent rebalancing without the burden of tax implications.

AI-driven tools enhance this process by monitoring positions and issuing alerts when allocations drift beyond acceptable thresholds. This ensures rebalancing occurs only when necessary, avoiding excessive transaction costs. This method aligns with best practices in active portfolio management, where research shows that annual rebalancing offers a risk-adjusted benefit of 51 basis points (0.51%) compared to the inefficiency of daily rebalancing.

Conclusion

Dynamic portfolio rebalancing serves as a risk-control mechanism, not a strategy for chasing returns. By systematically correcting portfolio drift, it ensures that the intended risk profile is preserved. This approach also enforces the disciplined principle of "sell high, buy low", reducing the influence of emotional decision-making.

Studies indicate that sentiment-driven dynamic portfolios outperform fixed-period rebalancing models and simple diversification strategies. For instance, annual rebalancing has been shown to deliver a risk-adjusted benefit equivalent to 51 basis points (0.51%).

Dynamic strategies - whether based on thresholds, hybrid models, or market conditions - offer traders the flexibility to respond to real-time market signals while staying aligned with their core risk objectives. This flexibility is especially useful in simulated proprietary trading environments, where strict drawdown limits and profit targets are non-negotiable. Additionally, essential tools for funded traders can save up to 50% of the time typically spent on manual portfolio management, allowing traders to concentrate on refining their strategies.

For those using virtual capital on platforms like For Traders, dynamic rebalancing is essential to maintaining key performance metrics such as the Sharpe and Sortino ratios. By integrating AI-powered risk management tools and real-time dashboards with platforms like DXTrade, TradeLocker, and cTrader, traders can execute systematic rebalancing efficiently and at a lower cost.

"The flexibility in adjusting the asset allocations according to investor sentiments improves realized portfolio performance." – ScienceDirect

This combination of discipline and adaptability transforms reactive portfolio management into a strategic advantage, equipping traders with the tools they need to succeed.

FAQs

How do I choose the right rebalance threshold (like ±5%)?

When deciding on a rebalance threshold, factors like risk tolerance, transaction costs, and market volatility play a key role. A tighter threshold, such as ±3-5%, might appeal to those who prefer minimizing risk, though it can lead to higher trading costs due to more frequent adjustments. On the other hand, a wider threshold like ±10% allows for greater portfolio drift but keeps trading activity - and costs - lower. A good starting point is ±5%, which you can fine-tune based on your comfort level with risk, expenses, and how markets are behaving.

When does dynamic rebalancing become too costly or too frequent?

Dynamic rebalancing can lose its appeal when transaction fees and taxes start to overshadow the advantages of keeping your portfolio's asset allocation on track. Rebalancing too frequently - say, every month - might rack up unnecessary costs without boosting performance, potentially eating into your long-term returns.

To strike the right balance, many experts suggest rebalancing either once a year or only when your asset mix drifts significantly from its target. This approach helps you sidestep excessive trading and minimizes tax-related inefficiencies.

Can I automate dynamic rebalancing on For Traders?

Yes, it's possible to set up dynamic rebalancing on For Traders by using automated systems or bots. These tools make it easier to manage your portfolio by automatically adjusting it based on your chosen settings. You can program them to rebalance at specific time intervals or in reaction to market changes, helping your strategy stay on track with your investment goals.

Related Blog Posts

Start Trading with For Traders

Join our platform to test your trading skills, trade virtual capital, and earn real profits. Access educational resources, advanced tools, and a supportive community to enhance your trading journey.

Start your Trading Challenge