Slippage is a common challenge in prop trading, where even small price differences between expected and executed trades can disrupt strategies and erode profits. Here's what you need to know:

Quick Tips to Minimize Slippage

Slippage is unavoidable but manageable with the right tools and strategies. Ignoring it can lead to live trading results that are 30–50% worse than backtests. Stay vigilant and plan for slippage to protect your performance.

Slippage Impact on Prop Trading: Costs, Causes, and Performance Metrics

Trading Slippage: How To Simulate And Minimize It

What Causes Slippage in Prop Trading?

To effectively address slippage, it’s essential to understand the factors behind it. Slippage typically stems from three main causes: market volatility, latency, and broker execution models.

Market Volatility and Liquidity Gaps

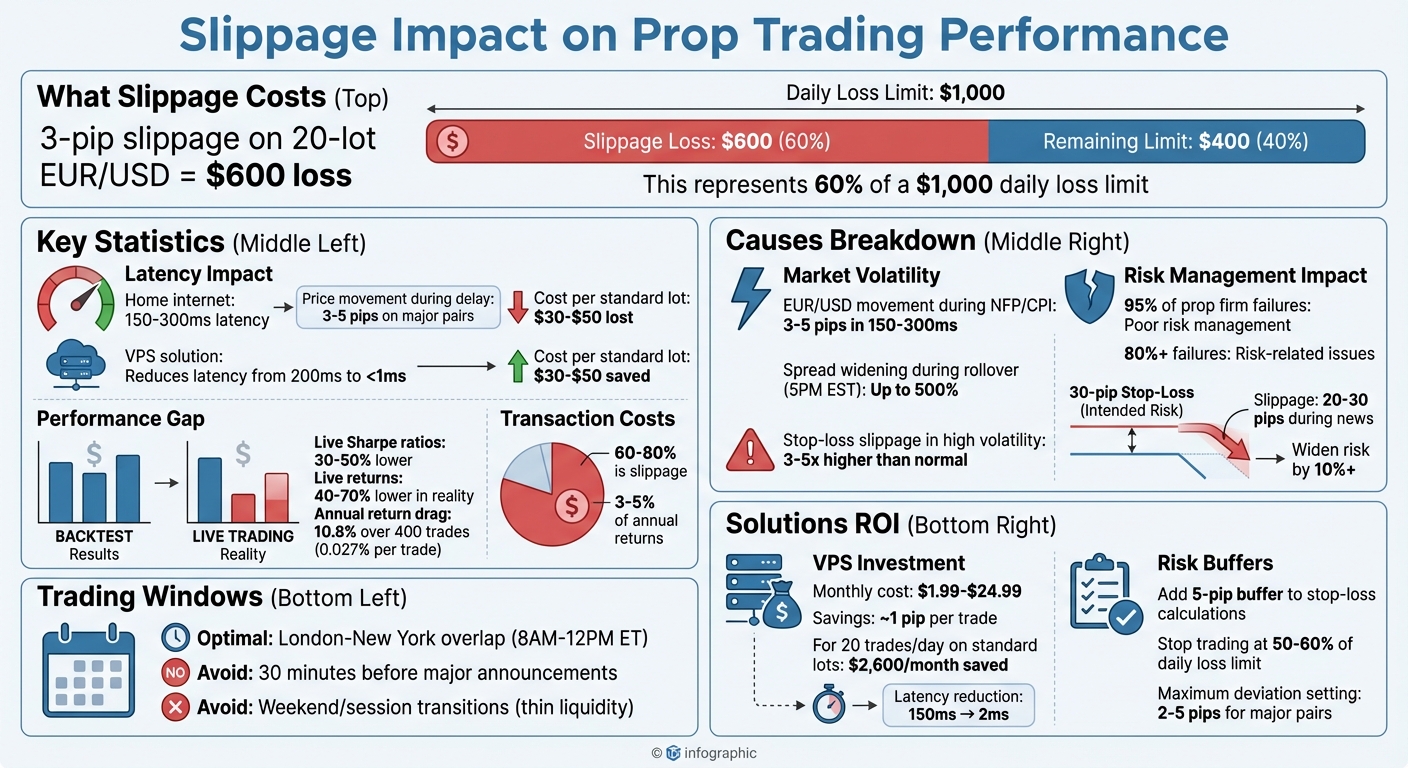

Slippage often happens when markets move faster than your order can be processed. This is especially common during high-impact events like Non-Farm Payrolls (NFP), Consumer Price Index (CPI) releases, or Federal Reserve announcements. For example, during these events, currency pairs such as EUR/USD can shift by 3–5 pips in just 150–300 milliseconds.

Low liquidity also plays a big role. During off-peak hours, weekends, or session transitions, the order book becomes thinner. If your order size exceeds the available volume at the best price, your broker may need to "walk the book", filling your trade at progressively worse prices.

"Slippage is a fundamental execution challenge... an unavoidable structural byproduct of how modern electronic markets match competing orders across fragmented liquidity pools."

Even exotic currency pairs face extreme conditions, particularly during the daily rollover window at 5:00 PM EST. During this time, spreads can widen by as much as 500% as liquidity providers temporarily pull back from the market.

Order Processing Delays and Latency

Latency refers to the time delay between placing an order and its execution. This delay creates a window where prices can fluctuate, exposing traders to slippage. For instance, a typical home internet connection with latency between 150–300 milliseconds can allow major currency pairs like EUR/USD to move 3–5 pips during that time.

Geographical distance also affects latency. If you’re trading from Los Angeles and your broker’s server is in London’s LD4 data center, the added travel time can lead to outdated prices and increase the risk of slippage or requotes. To combat this, many traders use low-latency VPS options hosted in the same data center as their broker. This setup can reduce latency dramatically - from around 200 milliseconds to under 1 millisecond - minimizing the chances of adverse price shifts.

Broker Execution Models and Their Role

The execution model used by your broker also determines how slippage impacts your trades. A-Book brokers (also known as STP or ECN) route orders directly to external liquidity providers. This approach exposes traders to real market slippage, which can be negative or occasionally positive if the market moves in your favor during order processing.

On the other hand, B-Book brokers (market makers) execute trades internally against their own inventory. While they might advertise fixed spreads or "zero slippage", these brokers often issue requotes during volatile conditions to protect their balance sheets. In extreme cases, this can even prevent trade execution altogether.

Prop trading firms often use simulated environments designed to closely replicate live market conditions. These platforms may include "Fair Market Value" clauses, which allow adjustments or cancellations of trades filled at unrealistic prices caused by data feed errors or extreme liquidity gaps during major news events.

Understanding your broker’s execution model helps you anticipate how slippage might affect your trades. Armed with this knowledge, you can fine-tune your strategy to better navigate the challenges of live trading. Up next, we’ll explore how these causes of slippage can impact profitability and trading risks. Managing these factors is a core part of risk rules for prop trading challenges that every funded trader must master.

How Slippage Affects Prop Trading Performance

Understanding slippage is essential in prop trading, where strict rules and tight limits can make even small deviations costly. Slippage doesn't just nibble away at profits - it can seriously disrupt your entire trading strategy.

Impact on Risk Management and Drawdown Limits

Slippage can wreak havoc on risk management, especially in environments with strict drawdown limits. When you place a market order, you’re asking for a specific price, but you’re not guaranteed to get it. That gap between your intended price and the actual execution can eat into your daily loss limit before the market even moves.

Stop-loss orders, which execute as stop market orders, ensure your trade gets closed but don’t promise a specific exit price. This becomes a problem during volatile times, like major news events (think NFP or CPI releases), where slippage can easily hit 20–30 pips. If you’ve set a 30-pip stop loss, this could widen your risk exposure by 10% or more, thanks to slippage and spreads.

Prop firms often calculate daily loss limits based on equity, not just realized profits or losses. This means a single poorly executed trade can take a big chunk out of your trading capital. It’s even more dangerous in trailing drawdown models, where gains don’t create extra breathing room. One bad fill could push you over the edge permanently.

To put it in perspective: 95% of prop firm evaluation failures come down to poor risk management, and over 80% are directly tied to risk-related issues. As Gary M., founder of Trader's Second Brain, explains:

"Getting funded is 20% strategy, 80% risk management."

To safeguard yourself, consider adding a 5-pip buffer to your stop-loss calculations when sizing positions. You can also set personal circuit breakers - stop trading once you’ve hit 50–60% of your firm’s daily loss limit. This gives you a cushion against unexpected slippage or sudden market spikes.

Erosion of Profitability in High-Slippage Environments

Beyond risk management, slippage directly chips away at profitability by adding unplanned costs to every trade. Each missed price level means you're starting at a disadvantage. For strategies relying on tight profit margins, this extra cost can quickly pile up.

Take a scalping strategy with a 1:2 risk-to-reward ratio, which only needs a 35% win rate to break even. Consistent slippage, however, can erode this edge, turning a winning strategy into a losing one. Poor fills widen stop distances and shrink profit potential, making it harder to stay profitable.

Real-world data backs this up. Live Sharpe ratios are often 30% to 50% lower than backtested results. High-turnover strategies, especially quantitative ones, can lose 3–5% of their annual returns to transaction costs, with slippage accounting for 60–80% of these costs for large institutional orders.

The gap between backtests and live trading - what’s often called the "backtest-to-live haircut" - is largely due to unrealistic assumptions about perfect fills. Quant Decoded sums it up well:

"Transaction costs are not a secondary concern but the primary determinant of whether a strategy is viable."

Psychological Strain on Traders

Slippage doesn’t just hurt your account - it messes with your head. After hours of careful analysis and patience, seeing your trade execute at a worse price than expected can be incredibly frustrating. This emotional strain often leads to bad decisions.

For traders transitioning from demo accounts to live trading, the difference is especially jarring. In demo environments, fills are instant and prices are clean. But in live markets, the "perfect fill illusion" disappears, leaving you questioning whether your strategy is flawed or if execution issues are to blame.

This creates what some call the "Prop Trader's Dilemma." A single trade with significant slippage can wipe out a large part of your daily loss limit, forcing you to decide whether to keep trading with less room for error or stop altogether. Even when you’ve done nothing wrong strategically, this uncertainty can lead to impulsive revenge trading, which often makes things worse.

Slippage can also erode confidence, making you hesitant to act on valid setups or tempting you into risky trades to recover losses. The key is to accept slippage as part of the trading landscape, not an anomaly. Here’s how you can adapt:

Next, we’ll explore strategies to tackle these slippage challenges effectively.

Strategies to Reduce Slippage

Now that you see how slippage can hurt your prop trading account, let’s explore some practical ways to minimize its impact. While you can’t eliminate slippage entirely, these strategies can help reduce it significantly.

Using Limit Orders and Maximum Deviation Settings

One effective way to manage slippage is by avoiding market orders. Market orders ensure your trade is executed immediately, but they provide no price protection. In contrast, limit orders protect you from unfavorable prices, though they don’t guarantee your trade will execute if the market moves away from your desired price.

For instance, if you want to buy EUR/USD at 1.0850, a limit order ensures you won’t pay more than that. If the market jumps to 1.0855 before your order is processed, the trade simply won’t execute. While you might miss the chance, you also avoid starting with a loss.

If you’re using platforms like MT4 or MT5, the Maximum Deviation setting can act as a safeguard for market orders. This feature lets you set a limit on how far the price can move before your order is rejected. For major pairs like EUR/USD, setting this to 2–5 pips offers a reasonable balance between speed and price protection. If the broker can’t fill your order within that range, it’s automatically canceled.

Here’s a quick comparison of order types:

Order Type

Price Control

Execution Guarantee

Best Use Case

High - guarantees price or better

None - may not fill

Entering positions in stable markets

None - accepts any available price

High - fills immediately

Urgent exits (use with Maximum Deviation)

Limits exit slippage to a set range

None - may not fill if price gaps

Protecting against large stop-loss slippage

Pairing the right order type with favorable trading conditions can help you keep slippage in check.

Optimizing Trading Conditions

The timing of your trades and the instruments you choose are just as important as the type of orders you use. Trading during high-liquidity periods reduces slippage because there’s more volume available. For forex majors, the best time is during the London-New York overlap - 8:00 AM to 12:00 PM ET - when both major markets are active.

Stick to liquid currency pairs like EUR/USD, GBP/USD, or USD/JPY. While exotic pairs might seem appealing with their larger price swings, their thin liquidity can cause even small trades to shift the market against you.

Another tip: steer clear of trading during major economic announcements. Close any open positions at least 15–30 minutes before events like Non-Farm Payroll (NFP) or Consumer Price Index (CPI) data releases. These moments often see liquidity dry up and spreads widen dramatically.

Leveraging Technology and Infrastructure

Once you’ve optimized your order types and trading hours, focus on reducing physical latency to further cut down on slippage. Your internet connection could be costing you money. A typical home connection has a latency of 150ms to 300ms - plenty of time for EUR/USD to move 3–5 pips before your order reaches the server. That’s roughly $30–$50 per standard lot.

Using a Virtual Private Server (VPS) can solve this issue. A VPS hosts your trading platform in the same data center as your broker’s servers, dramatically cutting down on latency. For example, if your broker operates out of Equinix LD4 in London or NY4 in New York, choose a VPS located in that exact facility. This setup can reduce latency from 200ms to just a few milliseconds.

The numbers speak for themselves: lowering latency from 150ms to 2ms can save about 1 pip of slippage per trade. For an automated strategy running 20 trades daily, that’s about $2,600 a month on standard lots. Considering that a VPS costs between $1.99 and $24.99 per month, the investment pays for itself quickly.

As FXNX aptly states:

"In the world of prop trading, milliseconds equal money."

To further reduce delays, optimize your trading platform by closing unused charts, disabling unnecessary custom indicators, and adjusting the "Max bars in chart" setting to lower processing demands. Every millisecond you save can make a difference in fast-moving markets.

Slippage in Prop Trading Challenges

In simulated prop trading evaluations on For Traders, slippage can be the deciding factor between success and failure. Many traders design strategies using backtesting tools that assume perfect fills at exact candle prices. This creates what’s often called the "perfect fill illusion", where a strategy appears profitable in theory but falters in actual trading.

The gap between backtested and live trading results is striking. Studies indicate that live trading returns are typically 40–70% lower than backtested results, largely because backtests often fail to account for slippage and latency. So, a strategy that seemed like it would easily hit a 9% profit target might barely squeak by - or worse, breach drawdown limits before achieving the goal.

Reconciling Backtested and Live Performance

Slippage plays a huge role in why backtested results often don’t translate to live trading. Most backtesting platforms assume perfect fills and unlimited liquidity, completely ignoring the execution gap. In reality, orders are routed through exchanges or liquidity providers, delayed by network latency (50–500ms), and filled at whatever price is available when they arrive.

As ASMR Education aptly puts it:

"A backtest that ignores [slippage] is not a test of a strategy; it is a test of a fantasy."

This issue is especially problematic for strategies with tight profit targets, which are common in prop trading challenges. Even a seemingly small slippage of 0.027% per trade can cause a 10.8% annual drag on performance over 400 trades. If your goal is a 25% annual return, that slippage alone eats up 43% of your profits.

Slippage is also asymmetrical - it tends to hurt more than help. You’re often slipped on both ends: entering trades during momentum and exiting during adverse moves. Stop-loss slippage during high-volatility periods can be 3–5 times higher than normal, completely throwing off your planned risk-to-reward ratios.

To bridge the gap between backtested and live performance, try this: export your last 100 trades and manually add 2 ticks of slippage to every entry and exit, plus 1 tick to each stop-loss. Recalculate your P&L. If your strategy turns unprofitable or your maximum drawdown exceeds the limits of your prop challenge, it’s time to tweak your approach.

These differences underline the importance of realistic evaluation methods when preparing for simulated challenges.

Tips for Prop Trading Challenge Participants

Given these discrepancies, traders need to adjust their strategies to account for slippage during prop challenges. Here are some practical steps to take:

James Mitchell, a trading systems developer, explains it well:

"The market doesn't owe you the price you want. It gives you the price it has. The difference between those two prices is called slippage, and it's always in the market's favor."

Keep in mind that For Traders challenges impose a strict 5% maximum drawdown limit. A large position slipped by just a few pips can eat up a big chunk of that buffer before the market even moves. To avoid this, keep position sizes conservative, especially during the volatile London-New York overlap or around major economic announcements when spreads can widen significantly.

Conclusion

Slippage is a persistent challenge in the world of prop trading, driven by factors like market volatility, liquidity gaps, and execution delays. These delays can lead to price discrepancies that eat into profit margins and disrupt risk-to-reward ratios, sometimes triggering strict drawdown limits before your position is fully realized.

The impact of slippage can be particularly damaging over time. Even minor price differences can erode a trading strategy's effectiveness, turning what seemed like a winning approach on paper into a losing one in live markets.

To mitigate slippage, traders must focus on proactive measures. Tools such as specific order types and maximum deviation settings are vital for navigating volatile periods and avoiding unfavorable fills. Using a VPS to minimize latency - cutting it from around 200 ms to under 1 ms - can also make a significant difference in reducing slippage-related losses.

"Slippage is the silent profit killer that separates the funded professionals from the perpetual 'reset' buyers"

Though slippage cannot be entirely avoided, understanding its causes and leveraging the right tools - like optimized order types, low-latency infrastructure, and careful position sizing - can help transform it into a manageable expense. For prop traders, mastering slippage management is a key step toward consistent, long-term success.

FAQs

How can I estimate slippage before I trade?

To get a handle on slippage, start by placing small test trades. This lets you compare the expected price with the actual execution price, giving you a clearer picture of potential discrepancies. Keep an eye on the bid-ask spread too - when the spread is wider, it often indicates a higher risk of slippage.

Another tool to consider is the Average True Range (ATR). While it won't directly measure slippage, it does provide insights into price volatility, which can indirectly affect execution. Lastly, pay attention to overall market conditions, especially liquidity and volatility, as these factors play a big role in shaping your trading outcomes.

When should I avoid trading to reduce slippage?

To reduce slippage, steer clear of trading during periods of high market volatility or when liquidity is low. These situations make it more likely for prices to shift between the time you place an order and when it’s executed. Instead, aim to trade during stable market hours when liquidity is abundant, and price movements tend to be steadier.

How do I add slippage into my backtests?

When incorporating slippage into your backtests, adjust trade prices to account for the gap between expected and actual execution prices. Most platforms allow you to set slippage parameters, such as a percentage-based adjustment or a fixed cost per trade. Alternatively, you can manually tweak the entry and exit prices. These adjustments aim to replicate real trading conditions more closely, making your backtests more reflective of actual market behavior.

Related Blog Posts

- Role of Leverage in Prop Trading Explained

- Is "overtrading" really bad? Read advice from skilled traders.

- Understanding Drawdown: Why It’s Crucial in Prop Trading

- What Makes Futures Trading Ideal for Prop Firms

{"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"How can I estimate slippage before I trade?","acceptedAnswer":{"@type":"Answer","text":"<p>To get a handle on slippage, start by placing small test trades. This lets you compare the <em>expected</em> price with the <em>actual</em> execution price, giving you a clearer picture of potential discrepancies. Keep an eye on the bid-ask spread too - when the spread is wider, it often indicates a higher risk of slippage.</p> <p>Another tool to consider is the Average True Range (ATR). While it won't directly measure slippage, it does provide insights into price volatility, which can indirectly affect execution. Lastly, pay attention to overall market conditions, especially liquidity and volatility, as these factors play a big role in shaping your trading outcomes.</p>"}},{"@type":"Question","name":"When should I avoid trading to reduce slippage?","acceptedAnswer":{"@type":"Answer","text":"<p>To reduce slippage, steer clear of trading during periods of high market volatility or when liquidity is low. These situations make it more likely for prices to shift between the time you place an order and when it’s executed. Instead, aim to trade during stable market hours when liquidity is abundant, and price movements tend to be steadier.</p>"}},{"@type":"Question","name":"How do I add slippage into my backtests?","acceptedAnswer":{"@type":"Answer","text":"<p>When incorporating slippage into your backtests, adjust trade prices to account for the gap between expected and actual execution prices. Most platforms allow you to set slippage parameters, such as a percentage-based adjustment or a fixed cost per trade. Alternatively, you can manually tweak the entry and exit prices. These adjustments aim to replicate real trading conditions more closely, making your backtests more reflective of actual market behavior.</p>"}}]}

Start Trading with For Traders

Join our platform to test your trading skills, trade virtual capital, and earn real profits. Access educational resources, advanced tools, and a supportive community to enhance your trading journey.

Start your Trading Challenge