If I had to cut this article down to one idea, it would be this: I should rebalance a virtual portfolio based on risk drift, not just the calendar.

A portfolio can look fine by weight while risk has already changed. In the article, that risk shift shows up through volatility, correlation, drawdown, position size, and prop-firm limits.

Here’s the short version:

- I watch volatility targets so exposure falls when markets get more volatile.

- I track correlation, because positions that move together can act like one big trade.

- I use drawdown triggers so I act before losses get too close to account limits.

- I set tolerance bands so I don’t trade on every small move.

- I link position sizing to portfolio rebalancing, instead of treating them as separate rules.

- I monitor often, but I only trade when a rule is hit.

- I write the whole plan down and backtest it across bull, bear, and crash periods.

A few numbers from the piece make the point fast:

- An unrebalanced 60/40 portfolio drifted close to 80/20 over time in one Vanguard example.

- During 2020–2021, a 60/40 mix moved to about 72/28 in under 18 months.

- A 5% drift band kept volatility near monthly rebalancing in one simulation, with less turnover than daily resets.

- In simulated prop accounts, daily drawdown limits of 3% to 4% mean I need rules that react before the next scheduled review.

Portfolio Rebalancing Explained | Strategies, Timing, & Risk Management

Quick comparison

| Method | What triggers it | Best use | Main issue |

|---|---|---|---|

| Calendar | Fixed date | Simple routine | Can miss fast risk drift |

| Tolerance band | Weight drift | Control trading frequency | Needs clear band rules |

| Drawdown trigger | Loss from peak | Tight loss limits, prop rules | Can fire during stress |

| Volatility target | Change in realized volatility | Keep portfolio risk steadier | Needs a tested lookback |

What I like about the article is its main point: rebalancing is not about chasing return. It is about keeping the portfolio close to the risk level I chose in the first place.

So if I’m running a demo or prop-style account, the basic playbook is simple: set a risk budget, use bands, watch volatility and correlation, respect drawdown limits, and test the plan before using it under pressure.

Why Risk-Based Rebalancing Outperforms Calendar-Only Rebalancing

Calendar rebalancing follows the clock. Risk-based rebalancing follows what the portfolio is actually doing. That gap matters a lot when volatility or correlations shift before the next scheduled rebalance. A date on the calendar can’t see that change, which is why time alone is a weak trigger.

The problem is simple: portfolios don’t drift on a neat schedule. Markets move when they move. During the 2020–2021 bull run, a standard 60/40 portfolio drifted to about 72/28 in less than 18 months. No trade was needed for the risk profile to change. It just happened as stocks ran ahead of bonds.

Risk-based rules watch the things that alter portfolio behavior in practice:

- volatility

- correlation

- drawdown

That matters because weights can look fine on paper while risk is quietly building underneath. Correlation risk is a good example. If assets start moving together more than before, the portfolio can become less diversified than it appears. And if leverage is in the mix, price moves can push exposure above target even when the allocation hasn’t been reset.

"The primary cost of infrequent rebalancing is risk elevation, not return reduction." - Quant Decoded

You can see the gap in both volatility and turnover:

| Rebalancing Strategy | Ann. Volatility (2000–2025) | Max Drawdown | Annual Turnover |

|---|---|---|---|

| Daily | 9.8% | -35.2% | 42% |

| Monthly | 10.0% | -35.6% | 7% |

| Quarterly | 10.2% | -36.1% | 4% |

| Annual | 10.9% | -37.4% | 1.5% |

| 5% Drift Band | 10.0% | -35.5% | 5% |

(Source: Quant Decoded simulation of a 60/40 US equity/bond portfolio)

The pattern is hard to miss. Waiting longer cuts turnover, but it also lets risk drift farther from target. Drift-band rules often land in a better middle ground in simulations: they keep risk closer to plan without trading as often as a rigid daily schedule.

Next: the rebalancing rules that keep risk tied to your account size and strategy.

1. Use For Traders to Test Risk Rules in a Simulated Environment

A simulated account is the fastest way to test risk rules before you put money on the line. For Traders gives you a place to do that, so you can pressure-test rebalancing rules during drawdowns and correlation spikes without touching live capital.

That matters because rules often look fine on paper, then fall apart when the market gets messy. In a simulated setting, you can run the same setup again and again and see if your process still holds when losses stack up or several positions start moving in the same direction.

For Traders applies a 3–4% daily drawdown limit, which makes it a useful place to test portfolio-level risk rules. That limit resets at midnight CET/CEST based on the higher of account balance or equity. If you practice around that reset over and over, you start building a simple but hard-to-fake habit: rebalance or close positions before the reset, not after.

You can also use the same setup to spot which assets tend to move together and should be managed as one unit. When correlation goes above +0.7, treat those instruments as one risk bucket. That sounds simple, but in live trading it's easy to miss. A virtual account gives you room to check whether your triggers are tight enough to protect the account or so loose that risk starts drifting.

| Risk Level | Purpose | Example Rule |

|---|---|---|

| Trade-level | Max loss on one trade | 1% of account per trade |

| Daily Drawdown | Max loss in one session | 3–4% of initial balance |

| Correlation Risk | Combined directional exposure | Max 2–3% across correlated assets |

Run the same scenario more than once until your bands, drawdown triggers, and correlation rules still hold up under stress. After that, turn those rules into a fixed risk budget you can use in a live-style setup.

2. Set a Clear Risk Budget for Your Portfolio

After you've tested your rules in a simulated account, put them into a fixed risk budget. That simply means setting a hard cap on exposure and loss so your simulated portfolio stays within the limits you planned for and doesn't break your risk rules.

Why does this matter? Because without a risk budget, a portfolio can quietly drift. A strong run feels great, but it can also push you into taking more risk than you meant to. And if you haven't set clear limits ahead of time, there's no obvious point where rebalancing should kick in.

Use drawdown thresholds to force action before losses get out of hand. In virtual or simulated prop trading settings, a 10% maximum drawdown is a common starting point:

| Drawdown Level | Recommended Action |

|---|---|

| 0–3% | Trade normally with standard position sizing |

| 3–5% | Reduce position size by 50%; trade only higher-quality setups |

| 5–7% | Use minimum size only; A+ setups only |

| 7%+ | Pause trading for 24 hours |

Source:

Exposure caps matter just as much. Keep any single position at no more than 10% of the portfolio, and cap total equity exposure at 70%. That way, a hot streak doesn't slowly turn your portfolio into something much more aggressive than you planned.

Once those limits are set, write them into a one-page Portfolio Rebalancing Policy Statement. Include your target weights, review timing, tolerance bands, and trigger rules.

3. Adjust Exposure Based on Volatility Targets

If your risk budget is the ceiling, volatility targeting is what helps you stay under it when markets start swinging.

The basic rule is simple: size positions by target volatility ÷ realized volatility. So if realized volatility is 2x your target, cut exposure by half.

Here’s why that matters. Fixed allocations don’t change when volatility jumps. That means portfolio risk can spike fast in a sell-off or crisis. Volatility targeting works differently. It keeps risk more stable by letting your allocation move with the market instead.

Before you lock in a trading rule, test both the target and the lookback period in your virtual account. Shorter lookbacks, like 20 days, tend to fit more volatile assets such as crypto. Longer lookbacks, like 60 days, tend to make more sense for stocks.

Data from simulations covering 2005 to 2025 showed that volatility targeting improved Sharpe ratios and reduced the 2008 drawdown from 37.0% to 21.4%.

To keep trading costs in check, rebalance only when exposure drifts by more than 10% from target.

Next, pair this with risk parity to spread exposure across assets and strategies.

4. Use Risk Parity Across Assets and Strategies

Risk parity spreads risk across positions, so one asset or strategy doesn't end up steering the whole portfolio. After you get total portfolio risk under control, the next job is deciding how to split that risk.

Here's the key point: equal dollars doesn't mean equal risk. If one holding swings a lot more than the others, it can drive a big chunk of your drawdown. Risk parity deals with that by weighting positions inversely to volatility, so each asset carries a similar share of the portfolio's risk.

This isn't just theory on paper. In a June 2024 QuantInsti study, risk parity beat equal weighting on Sharpe ratio, return, volatility, and drawdown across the Dow 30. That's why it works well as a practical rebalancing rule.

A simple way to test it is to compare equal weighting with inverse-volatility weighting in your virtual account using a 20-day rolling window. Then use what you find to set your rebalance rule and measure it against your volatility target.

5. Use Tolerance Bands to Avoid Over-Rebalancing

After you set target weights, the next step is deciding when drift is big enough to justify a trade.

That’s where tolerance bands come in.

Risk parity tells you the mix you want. Tolerance bands tell you when to step in and reset it. If you rebalance too often, you can pile up trading costs for no good reason. Bands solve that by setting clear limits for how far allocations can drift before you act.

A common institutional standard is the 5/25 Rule: rebalance when an asset class moves 5 percentage points away from its target weight, or when a position shifts by 25% of its target weight - whichever happens first.

For example:

- A 60% equity target would trigger a rebalance at 55% or 65%.

- A 10% satellite position would trigger at 7.5% or 12.5%.

Use absolute bands for core holdings and relative bands for smaller satellite positions. That setup makes sense because relative bands scale better with position size. A small holding can swing a lot in percentage terms, so using the same absolute rule for everything can get clunky fast.

A 2007 study by Gobind Daryanani found that a 20% relative threshold did the best job of balancing risk control with return efficiency.

The key idea is simple: rebalance only when a band is crossed. That keeps your trades tied to risk instead of the calendar.

6. Trigger Rebalancing From Drawdowns, Not Just Dates

When drift is small, bands do the job. But when losses start to speed up, drawdown triggers should take over. In practice, that means drawdown - not the calendar - is the better signal for portfolio action.

Drawdown-triggered rebalancing uses losses as the cue to act, not fixed dates. And the data backs that up. Threshold-based rebalancing posts a Sharpe ratio of 0.46, versus 0.34 for annual calendar rebalancing. On top of that, systematic rebalancing has been shown to cut maximum drawdown by 5 to 8 percentage points compared with a portfolio that is never rebalanced.

A simple rule set looks like this:

- Under 5% drift: monitor only

- 5% to 10% drift: rebalance

- Over 10% drift: rebalance at once

For virtual prop accounts, the line is even tighter. Daily drawdown limits are often just 3% to 4%, so they need to be treated as a hard stop. If that limit gets hit, review position sizes and risk limits before the next session.

A hybrid rule usually makes the most sense: check the portfolio every quarter, but step in right away if a drawdown or drift threshold gets hit first. Pair those drawdown triggers with position sizing rules so one bad trade doesn't throw the whole portfolio out of shape.

7. Connect Position Sizing Rules to Portfolio Rebalancing

Drawdown rules work best when each position fits the same risk budget. position sizing tools and rebalancing are just two layers of the same risk control. If those two parts aren't linked, risk can sneak up on you.

The biggest issue is drift. Even if each trade follows your size cap, total portfolio risk can still drift when position sizing isn't tied to rebalancing.

A simple fix: use your sizing limit as a rebalance trigger. If any position moves above its risk budget, trim it back. For volatile assets like crypto, size positions by their share of portfolio risk, not just by dollar weight. A position can look small in dollar terms and still carry a lot of risk if its volatility is high.

One of the simplest ways to tie sizing to rebalancing is with portfolio heat - the total percentage of your account you would lose if every open position hit its stop at the same time. Use portfolio heat as your final position-sizing check. Keeping total heat below 6% gives you a clear, measurable link between trade-level sizing and your portfolio-level risk cap. If portfolio heat gets close to that limit, rebalance right away.

8. Monitor More Often Than You Trade

Once your bands and drawdown triggers are in place, monitoring shows you when they matter. Monitoring spots risk drift. Rebalancing puts risk back in line. Those are two separate calls, and it helps to keep them that way.

Check your risk metrics every month, but only rebalance when a band or drawdown rule is actually breached. That way, you stay alert without piling on trades you don't need. In rough markets, clear trigger rules matter even more. They take the emotion out of the moment.

A simple setup works well:

- One rule for when you review

- One rule for when you trade

Without that written policy, it's easy to talk yourself into a trade based on what the market feels like instead of what the numbers say.

Virtual accounts can help here, too. Log each time a threshold would have triggered a trade, then check whether that trigger rate makes sense for your cost structure. If the rules fire too often, widen the bands. Those logs can also show whether your rules match your account limits.

9. Match Rebalancing Rules to Simulated Prop Account Constraints

Rebalancing in a simulated prop account has to fit the firm's hard rules: loss limits, drawdown caps, and position limits. If your plan ignores those guardrails, a sharp move can push you into a rule break fast. So the math behind your rebalance matters just as much as the limit itself.

Most prop firms track drawdown on real-time equity, not just closed balance. That includes unrealized P&L, which means floating losses count right away. In plain English, your account can hit a danger zone before your planned rebalance date even arrives.

Because of that, don't base rebalancing on account balance alone. Base it on remaining drawdown room. That's the number that tells you how much risk you can still carry without running into the firm's cap. And when you rebalance, leave some buffer. Getting too close to the hard limit is asking for trouble during a volatile session.

A good rule of thumb is to set your own daily stop at about 60% of the firm's daily loss limit. That gives you breathing room if the market gets jumpy or slippage hits harder than expected. It also keeps position sizing tied to the firm's rules instead of treating them like an afterthought.

As drawdown gets worse, tighten risk in steps instead of guessing on the fly:

- At 50% of max drawdown, cut position size by half

- At 75%, reduce size by 75% and take only your highest-conviction setups

- At 90%, stop trading and reassess

The same idea applies to trades that tend to move together. If several positions are highly correlated, don't size them as if each one stands alone. Treat them as one risk unit when you size and rebalance. That way, you're measuring the risk you actually have on the book, not the risk you wish you had.

10. Write Down and Backtest Your Rebalancing Plan

Once your risk budgets, bands, and drawdown rules are in place, put them into one written plan. If a rebalancing plan can't be tested, it isn't ready.

Start with a plain rule set: target weights, bands, triggers, sizing, and drawdown caps. Add a crash rule too. That means a set response for extreme moves, like waiting 48 hours before rebalancing after a sharp sell-off. Then test those rules against past market data.

This is where the plan either holds up or falls apart. A Vanguard study found that annual rebalancing slightly lowers return, but it also cuts volatility and drawdown in a meaningful way when compared with not rebalancing at all. A 5% threshold method can cut turnover by 45% versus quarterly rebalancing while keeping 92% of the risk-cutting effect. If the plan only looks good with perfect fills and zero slippage, that's a red flag.

Run the test across different market regimes:

- Bull markets

- Bear markets

- Range-bound periods

- The 2008 financial crisis

- The 2020 COVID crash

- The 2022 inflationary period

Then review the numbers that matter: Sharpe ratio, maximum drawdown, turnover, and rule violations. If the plan breaks down in any one regime, that's your cue to tighten the rules.

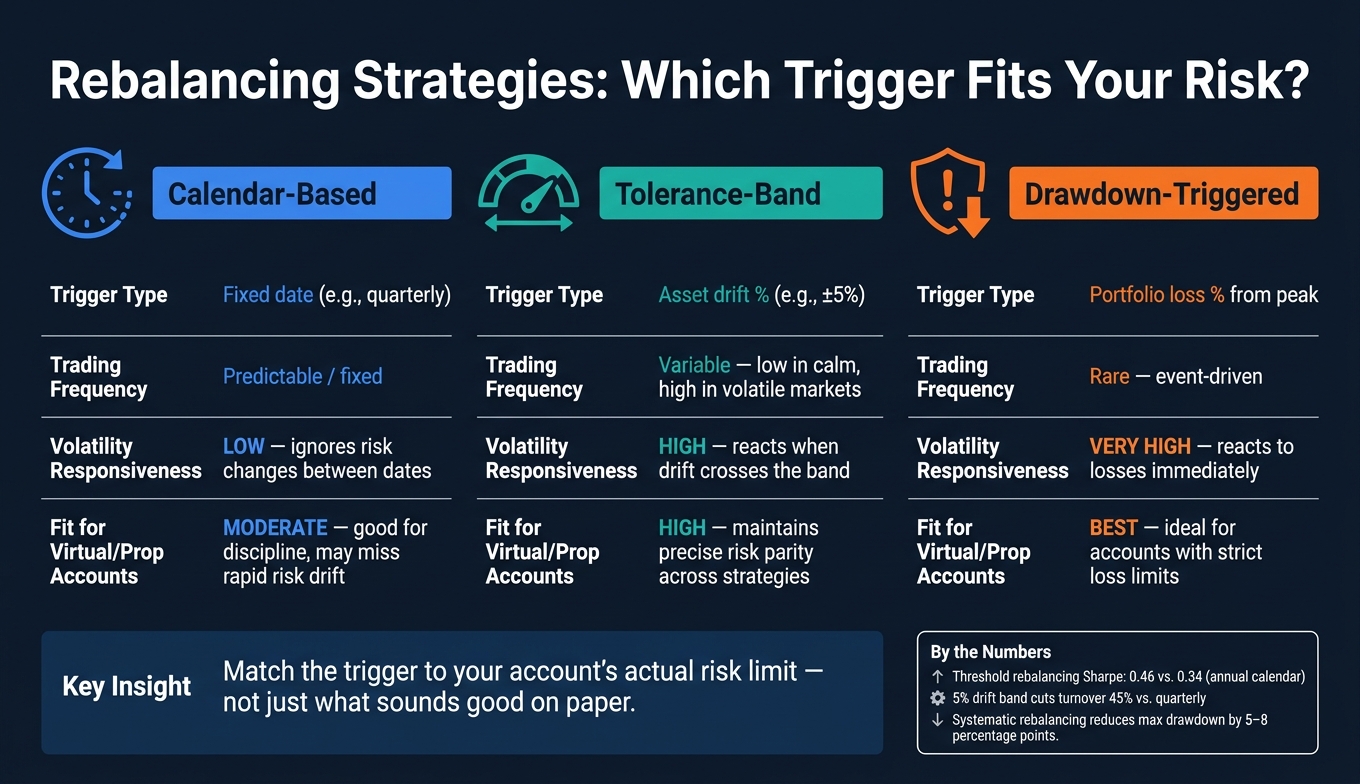

Calendar vs. Band vs. Drawdown Rebalancing: A Quick Comparison

Rebalancing Strategies Compared: Calendar vs. Band vs. Drawdown

Use the table below to match each rebalancing trigger to the risk problem it solves.

| Framework | Trigger Type | Trading Frequency | Volatility Responsiveness | Fit for Virtual/Prop Accounts |

|---|---|---|---|---|

| Calendar-Based | Fixed date (e.g., quarterly) | Predictable/fixed | Low - ignores risk changes between dates | Moderate - good for discipline but may miss rapid risk drift |

| Tolerance-Band | Asset drift % (e.g., ±5%) | Variable - low in calm, high in volatile markets | High - reacts when drift crosses the band | High - maintains precise risk parity across strategies |

| Drawdown-Triggered | Portfolio loss % from peak | Rare - event-driven | Very high - reacts to losses immediately | Best for accounts with strict loss limits |

Use the table to pick the simplest rule that fits your risk control problem.

Calendar-based rebalancing is easy to run, but it can be slow to react when risk shifts between scheduled dates.

Tolerance-band rebalancing controls drift as it happens, so risk stays closer to target without turning every small move into a trade.

Drawdown-triggered rebalancing is the most defensive option because it responds to losses, not the calendar.

The hard part isn't choosing a rule that sounds good on paper. It's matching the trigger to the account's actual risk limit.

Once the framework is set, the next place things often go wrong is execution.

Common Rebalancing Mistakes in Virtual Portfolios

A solid rebalancing plan can still go off the rails if the execution is messy. That's the catch: even a good rule stops working when small habits creep in and bend your risk over time.

One common mistake is rebalancing back to neat dollar weights without looking at how each position behaves. Two holdings can sit at the same portfolio percentage and still carry very different levels of volatility or move in lockstep with other assets. So a clean split on paper can still leave you with uneven risk. The goal isn't to make the allocation look tidy. It's to bring risk contribution back in line.

Another issue is taking fund labels at face value. Names can be misleading. A global equity fund and a tech-heavy growth fund may sound different, but they can still hold many of the same mega-cap stocks. If that's the case, rebalancing by allocation percentage alone won't fix the actual concentration. Rebalancing tends to work best when the assets involved have low correlation.

It's also easy to rebalance too often. Not every move matters. Sometimes drift is just noise, not a real shift in portfolio risk. That's why tolerance bands matter. They help screen out small changes that don't meaningfully alter your risk profile.

And if you're using a virtual portfolio, don't treat it like a game. Handle virtual capital the same way you'd handle live capital. Use the same risk management rules, position sizing, and rebalancing strategies you would use with real money. That kind of discipline keeps your simulated habits in step with how you'd trade when actual cash is on the line.

Conclusion

Effective rebalancing isn't about the calendar. It's about actual risk.

The best framework is usually the one you can define, test, and stick to when the pressure hits. Set one clear rule set for your risk budget, volatility, and drawdown. This is especially critical when applying crypto strategies for funded accounts where volatility is heightened. Then use calendar check-ins as a backup, not the main trigger.

Before you use those rules in a live account, test them in a simulated one. For Traders lets you stress-test your rules before live trading.

In virtual portfolios, the best rebalancing plans are simple, tested, and built to keep risk where you intended.

FAQs

How do I measure risk drift in a virtual portfolio?

Calculate the gap between each asset’s current weight and its target allocation.

To get the current weight, divide the asset’s current value by the total portfolio value. Then subtract the target percentage from that result.

- A positive number means the asset is overweight.

- A negative number means the asset is underweight.

For clean tracking, use prices from the same valuation date.

What tolerance band should I start with?

A common starting point is 5 percentage points away from your target allocation. Another option is the 5/25 rule: rebalance when an asset moves by 5 percentage points or 25% of its target weight, whichever happens first.

If you hold higher-volatility assets, Average True Range can help you set a moving threshold and cut down on extra trading. The goal is to manage risk by keeping your exposure in line with your original objectives.

When should drawdown triggers override my rebalance schedule?

Prioritize a drawdown trigger over scheduled rebalancing when your total portfolio value drops 10% below its peak. Think of it as a safety net: it calls for an immediate rebalance to lock in losses and help stop them from snowballing.

This rule helps keep your portfolio in line with your risk tolerance during sharp market swings, no matter what your usual rebalancing schedule looks like.

Related Blog Posts

Start Trading with For Traders

Join our platform to test your trading skills, trade virtual capital, and earn real profits. Access educational resources, advanced tools, and a supportive community to enhance your trading journey.

Start your Trading Challenge